The Difference Between Flood Cover and Storm Damage Cover

Published 20 March 2026

One of the most significant insurance misunderstandings in Australia is the distinction between flood cover and storm damage cover. These two types of water-related insurance cover different causes of damage, and a policy that covers one may explicitly exclude the other.

Getting this distinction wrong can leave a homeowner facing tens of thousands of dollars in uninsured repair costs following a water damage event.

Storm Damage Cover: What It Covers

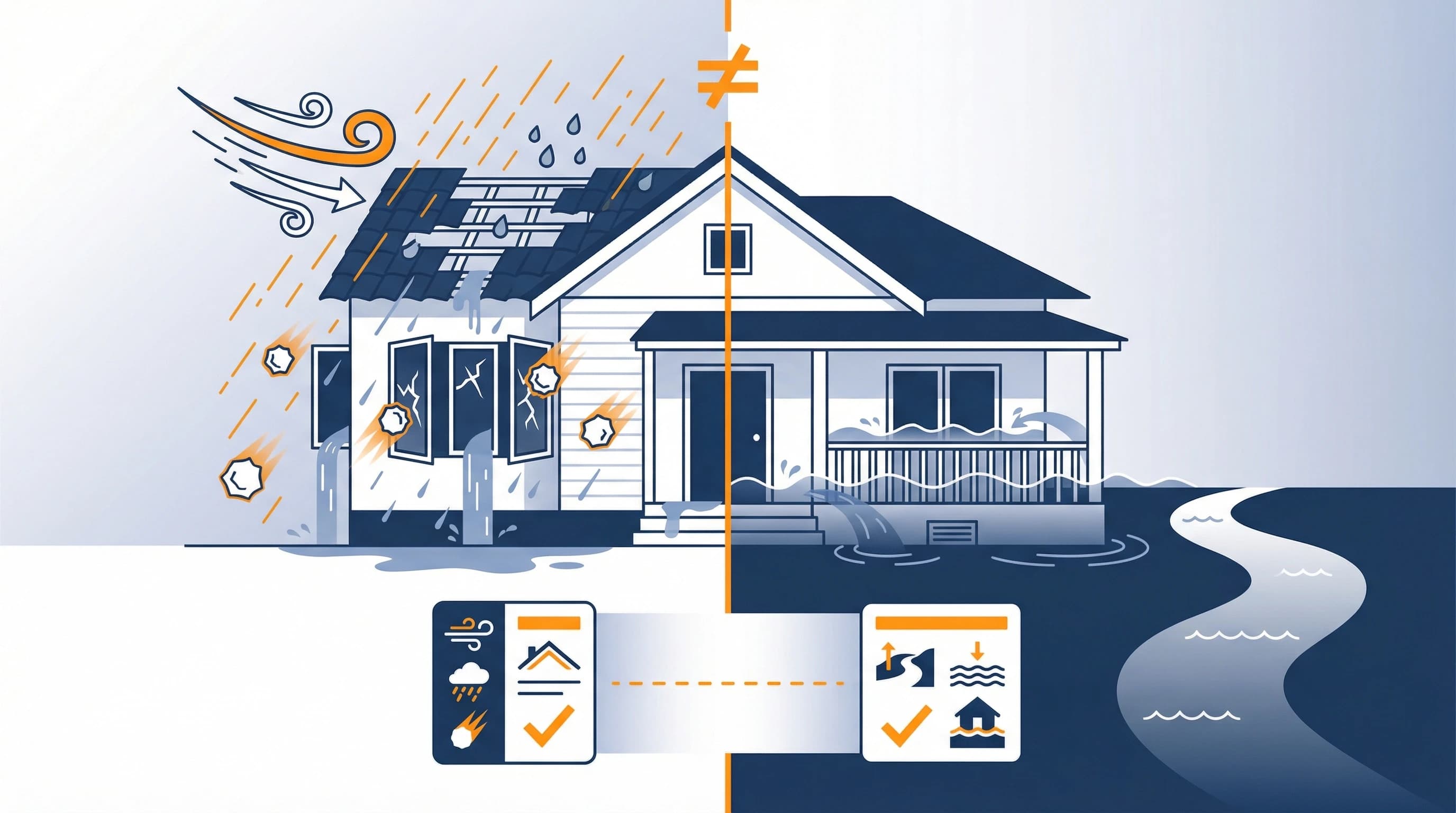

Storm damage cover, which is typically included as standard in Australian building and contents policies, covers damage caused by wind, hail, lightning, and the associated water entry caused directly by storm action. Examples include rain entering through a roof damaged by storm winds, water driven through doors or windows by extreme wind pressure, and hail damage to roofing, windows, and external cladding.

The key characteristic of storm damage is that the water entry is caused by the storm's direct physical action on the building, not by the accumulation or flow of water on the ground.

Flood Cover: What It Covers

Flood cover applies to damage caused by water overflowing from rivers, creeks, lakes, or other natural waterways, or by stormwater runoff that moves across land in the patterns associated with flooding.

The Insurance Council of Australia defines flood specifically as "the covering of normally dry land by water that has escaped or been released from the normal confines of any lake, river, creek or other natural watercourse, whether or not altered or modified, or any reservoir, canal or dam."

Crucially, overland flow flooding (stormwater runoff moving across the surface) may fall under either storm damage or flood cover depending on the specific policy wording. Some policies cover overland flow under their storm damage provisions. Others classify it as flood and require a separate flood cover endorsement.

The Policy Wording Matters Enormously

Following the 2011 Brisbane floods, the Insurance Council of Australia noted that claims disputes arose from differing interpretations of whether specific damage events were "flood" or "storm surge" or "stormwater," terms that different policies defined differently.

From 2012, ASIC and the Insurance Council worked toward standardising flood definitions in personal lines insurance policies. However, policies still vary in their scope and exclusions, and the specific wording of your policy remains critical.

Before purchasing any property with a flood overlay designation, or any property near a creek, river, or in a low-lying area, read the insurance product disclosure statement (PDS) specifically for flood definitions and exclusions. If the distinction between flood cover and storm damage cover is unclear, ask the insurer in writing to clarify whether the specific risk profile of the property you are purchasing is covered.

Pre-Purchase Insurance Research

As with all insurance research discussed in this series, the right time to investigate is before you make an offer, not after settlement. A PropDex due diligence report gives you the flood overlay status of any property, which is the starting point for a targeted insurance investigation.

If a property carries a creek flood overlay or Brisbane River flood planning area designation, you should specifically confirm that any policy you are comparing includes flood inundation cover under the relevant flood definition, not just storm damage.

Visit propdextest.com.au to check the flood overlay status of any property before beginning your insurance research.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.